What is the Asian financial crisis?

The Asian financial crisis was a financial, currency and economic crisis in East Asia between 1997 and 1998. It began in Thailand in March 1997 and spread throughout Southeast Asia to the so-called tiger and panther economies.

What is the Asian Financial Crisis?

Southeast Asian countries were characterised by a strong economic boom in the phase prior to the crisis. Access to cheap labour in the region had led, in particular, to European and Japanese companies outsourcing parts of the value chain to this region, which further boosted the economy there. The growth rates of countries such as Indonesia, Malaysia or Thailand averaged between 5% and 9% annually from 1990 to 1996, thus outperforming the growth of most industrialised nations. This strong growth also earned the countries the title of "Tiger economies". Thailand aimed to make Bangkok the financial hub of Southeast Asia and encouraged the establishment of financial intermediaries in the city.

However, the strong economic growth was also accompanied by structural problems, which initially went unnoticed. Thus, this phase was characterised by an extreme growth in credit volume, which was 8% to 10% above the countries' GDP growth. Huge loans were granted, whereby the lending criteria were handled very generously. This stimulated high investments in the stock and real estate markets of the Tiger economies, and prices soared. The growth also attracted the interest of some industrialised nations, which made high investments and granted loans. This became problematic in that the foreign debt of the Asian countries, issued in foreign currencies (mostly US dollars), far exceeded the countries' own foreign exchange reserves. Inadequately functioning supervisory authorities were unable to oversee the accumulating mountain of debt, and a large proportion of the banks affected had an equity ratio that was significantly too low. In addition, many Asian currencies were artificially pegged to the US dollar, which ultimately acted as one of the catalysts for the crisis. Even when the 1990s were particularly characterised by economic growth in the US, Asian central banks held on to the currency peg.

In 1997, when the first financial institutions in Thailand were unable to repay their loans due to cash shortages and had to take out new loans to pay their debts, the house of cards began to crumble. Thailand's central bank secretly provided liquidity to affected companies but was no longer able to pay its own accumulated debts from central bank reserves. As a result, Thailand abandoned its currency peg to the US dollar, causing the Thai Baht to lose between 15% and 20% of its value within a very short space of time. This drastic currency devaluation caused the US dollar-denominated debt of Thai companies to rise, meaning they could no longer meet their obligations. Shortly afterwards, other Asian countries, such as Singapore or Hong Kong, also suffered severe collapses in their respective currencies. The once strong Tiger economies now had enormous foreign debts that they could no longer service. Thailand alone had 90 billion US dollars in foreign debt at the time, and Indonesia had as much as 113 billion US dollars. As a consequence, real estate prices and shares in the affected countries also fell drastically.

Source: Ginmon, MSCI; As of: 30/06/2021

Only the intervention of the World Bank and the International Monetary Fund (IMF), which approved several major aid packages for the region, prevented an even deeper collapse of the economy. In order to defuse the situation, the World Bank responded with the highest loan commitments in its history to date, namely a sum of 28.6 billion US dollars.

Impact on Tiger Economies and Industrialised Nations

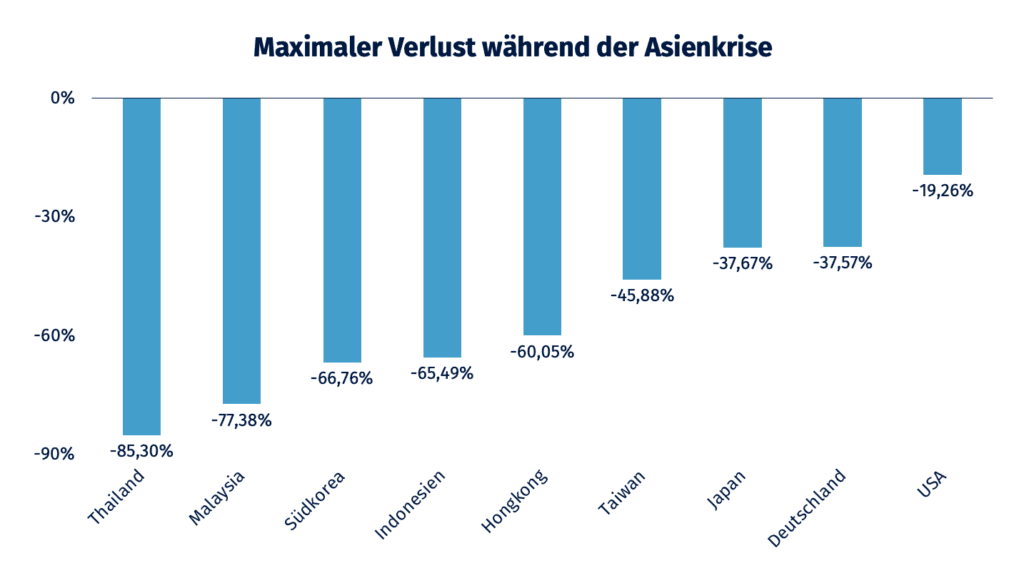

As a result of the crisis, several million people in Southeast Asia lost their jobs. In Indonesia, the unemployment rate doubled to almost 10%, and in South Korea, it rose to approximately 7%. However, Thailand was hit particularly hard. The country had achieved almost full employment before the crisis; by the end of 1997, there were around 1.2 million or 3.4 percent unemployed. But larger economies were not spared either. Japan, which was already struggling and faced a renewed slide back into recession, was particularly affected. The Japanese Nikkei lost over 7,000 points or almost 40% between July 1997 and October 1998. Russia, which already had problems with an immense budget deficit, the low price of crude oil at the time, and President Yeltsin's health issues, lost almost four-fifths of its value by mid-1998. This was followed by a devaluation of the Russian currency by over 50%, causing the entire Russian economy to collapse.